mike smitka

I made a short presentation as a component of board education for a local bank. The president was curious about Brexit, so I used that as a point of departure. What follows are thumbnails of slides; I add several at the end that (as expected) I did not get to during my talk.

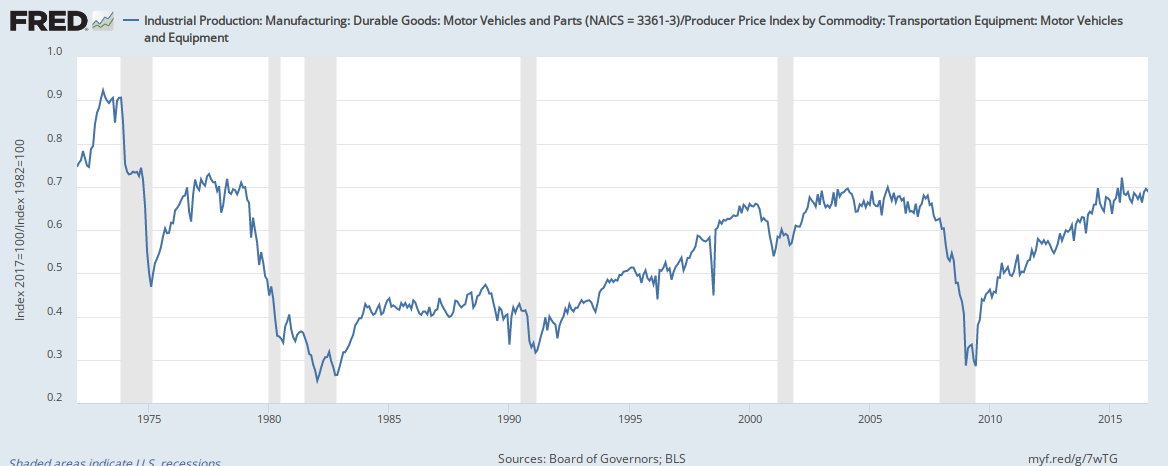

First, I began by emphasizing that there is no business cycle, as emphasized in a previous posting on this blog. By chance in the immediate aftermath of WWII the US had 3 recessions with similar timing, but that's not happened since. Just because we've gone 7 years without a recession doesn't mean that one is more likely in the next year. Furthermore, the apparent causes vary, so predicting on the basis of past recessions is pointless. Now once a recession has begun, then certain changes occur – but those can also arise without a recession being underway. So it is possible to calculate recession probabilities, but those are weak and at best provide information on the next several quarters.