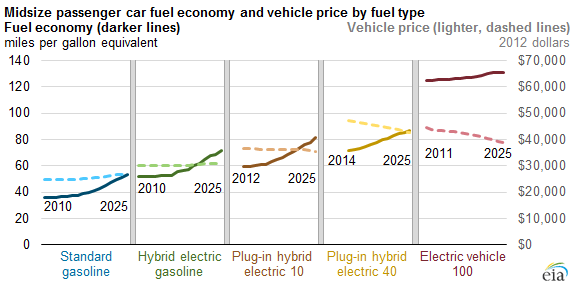

As emphasized in Chapter 11 of Smitka & Warrian (up on Amazon Jan 1st!), battery electric vehicles (BEVs) offer many efficiency benefits relative to vehicles powered by an ICE (internal combustion engine). However, this benefit comes with an up-front cost premium that means that, absent subsidies, they fail to provide a value proposition to purchasers. There is no evidence that will change by 2020.

One aspect is that ICEs continue to improve. A quick glance at the Automotive News PACE Awards finalists for 2016-17 shows that 11 of the 34 innovations up for this year's awards improve ICE efficiency. (Winners will be announced in a black-tie event at the Fisher Theater in Detroit on Monday, April 3rd, just before the start of the big annual Society of Automotive Engineers convention. Yours truly will be in attendance.) So while the cost of battery packs continues to fall, and density to increase, they face a moving target. Turbochargers are widespread, start-stop systems are more robust, parasitic losses are being cut as electric motors replace hydraulics, and variable compression systems are starting to launch.

...this is not the time to be launching a new sedan...

Furthermore, there's some indication that the current approaches to Li-ion chemistry are reaching their limits, though the best lab technologies are years from commercial production so incremental improvement will continue apace. Similarly, economies of scale in cell and battery pack are less than expected, evidenced by the construction of multiple small plants. My reading is that costs bottom out around 100,000 vehicles worth of battery packs a year. Now today no single model is at that point, but that day is not far off. Furthermore, battery margins aren't great, so it's not as though car companies pay exorbitant prices.

In other words, manufacturing isn't like internet businesses, where up-front development is a significant part of overall costs and hence every additional user improves profitability. Elon Musk is a victim of the old and mistaken Stalinist belief that bigger is always better. In contrast there are only a handful of "fine chemical" producers, which is where DOE analysis suggests the profits lie. But that's not the end of the business that Tesla is in, nor is it the focus of the battery joint ventures of Nissan and others.

That leaves two markets for electric vehicles: the luxury end, where price does not dominate the purchase decision, much less fuel efficiency. There other is as a "compliance car" made to satisfy one or another regulatory constraint.

| Model | Announcement | Delivery |

| Model S | June 2008 | June 2012 |

| Model X | Feb 2012 | Sept 2015 |

| Model 3 | July 2014 | ? late 2017 ? |

Tesla did very well in the $100K end of the market. Rather than supporting the Model S with a full redesign, Musk is instead moving downmarket. Slowly. After all, the company has limited engineering resources, and so can only come out with a new car once in 3 years. (They are promising an earlier date for the Model 3.) Unlike Jaguar, which will use the experienced contract assembler Magna Steyr for the 2018 launch of its I-Pace electric SUV, Tesla insists on going it alone. That eats up capital it could better use to replace its high-end product, and results in slow and late launches, replete with quality glitches.

So what will the market for the Tesla Model 3 be like? The bottom line is, not very good. First, direct subsidies are under attack (though what if anything the current US administration will actually do defies prediction). That is critical for sales of the Model 3, because sales targets transcend the volume the luxury market can generate. Then there are ZEV emission credits and more generally a car's contribution to meeting CAFE restriction. Tesla can't itself use ZEV credits; they need to sell them. And because they sell no fuel-gulping pickup trucks, what happens to CAFE is not directly relevant. Indirectly, though, the launch of the GM Bolt cuts into the ZEV market, and Trump's promised relaxation of CAFE requirements will shift the overall market even further away from the sedan segment. (Using BEA data, in Feb 2017 trucks ran at 11.2 mil SAAR, cars at 6.3 million.) This is not the time to be launching a new sedan, and Trump is promising to make the market less favorable. California is important enough to GM that they need to sell Bolts there to let them sell more high-margin SUVs and pickups. The compliance car market is not relevant for Tesla.

Then there are gas prices. Saudi Arabia would like OPEC to cut output, but is in no position to do so unilaterally. It provides subsidies to keep its population (and ever-larger royal family) happy, and is running a deficit. It desperately needs revenue, but with only a 10% share of the global market – and US tight shale output staying stubbornly high – a cut in output results in a less-than-proportional rise in price. Even with inelastic demand (say, -0.3), revenue falls. So it needs to keep pumping. Nor are US drivers helping, as Bloomberg points out. That makes it even harder to sell a BEV on the basis of their savings on gasoline purchases.

..Tesla investors are set to learn the hard way...

Now I've no doubt that the Model 3 will be a nice car, though even if it does carry a $35,000 list price, you won't be able to find one that isn't loaded. Since on the basis of history there's every reason to believe that initial production volumes will be quite low, we'll be regaled with stories of high demand, cars snapped up as fast as they can be produced. But can they sell 100,000 in 2018? I doubt it, and a mid-sized car in the volume segment won't deliver high margins in a market where everyone wants a truck. Meanwhile the Chevy Bolt will have been out for a full year, the Nissan Leaf updated and BEV subsidies in China pared. Tesla will have to be very generous on the trade-ins they accept to keep sales flowing. They can bury that in their financial statements for a while. Those in the auto industry know how that ends. Tesla investors are set to learn the hard way.

note that Tesla just raised an additional $1 billion in cash

bibliography

Chung, D., Elgqvist, E., & Santhanagopalan, S. (2016). Automotive Lithium-ion Battery (LIB) Cell Manufacturing: Regional Cost Structures and Supply Chain Considerations (No. NREL/PR-6A50-63354 Prepared under Task No. VTP2.6B01). CEMAC (Clean Energy Manufacturing Analysis Center).

Martin, R. (2016). Why We Still Don’t Have Better Batteries. MIT Technology Review, 119(6), 22–22.